Razor's Edge: Sprout Post-Mortem

So Sprout...

- Missed their Q4 internal revenue target despite rolling out a significant price hike on a 50% of ARR monthly cohort on Dec 1 vs Jan 1 to avoid notably missing their ARR target

- They basically missed the Q1 target rev guide internal and actually missed street on Q2 notably

- They missed every important kpi on Q1

- $50k+ customers adds were down 60% from same time last year and worst number in 3 years

- They added 50% less Social Studio customers than Q4

- Their DBNR, which is reported on an ARR basis, dropped 400bps in 2022 to 108% with the Dec hike included. Without the last second increase, the number was tracking for one of the worst yr/yr declines in public SaaS.

- Their existing guide requires them to achieve 75% of their ARR growth for 2023 in Q3/Q4 and to add 87% more ARR in those two quarters then they did in 2022 when the salesforce migrations ramped and they took notable pricing on existing customers as well as raised new pricing significantly ahead of Social Studio migration ramp

- And this is all occurring during the worst overall demand environment in software since the dotcom bubble burst

So, what does Sprout management do?

They raise their annual ARR target by 25bps!

Yes, 25bps!

Had they changed nothing they were gonna get slammed, but optically doing this makes you look like you are the most tone deaf management team in the history of SaaS.

As for the conference call, things just got worse.

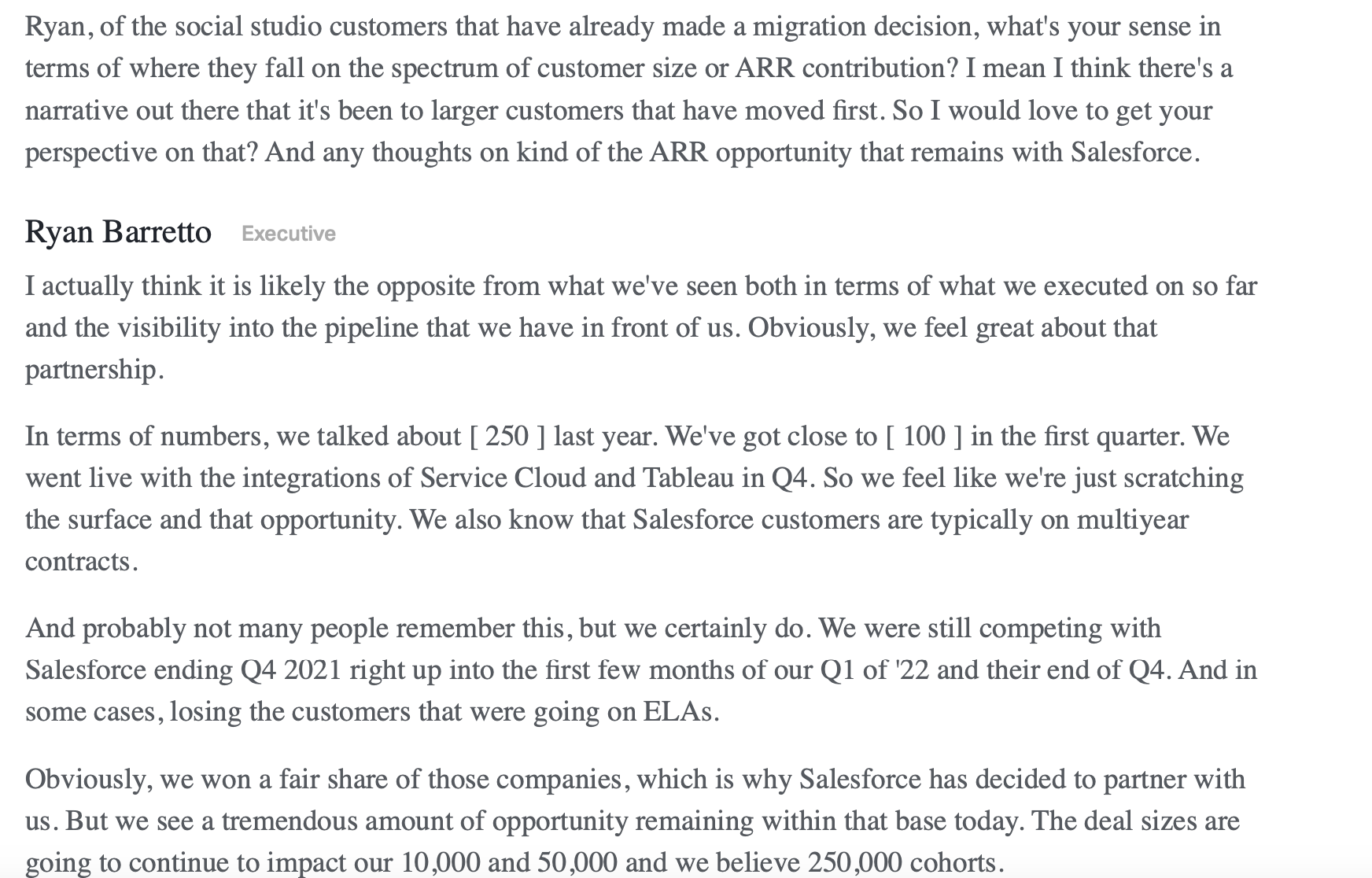

Here is a question on Social Studio..

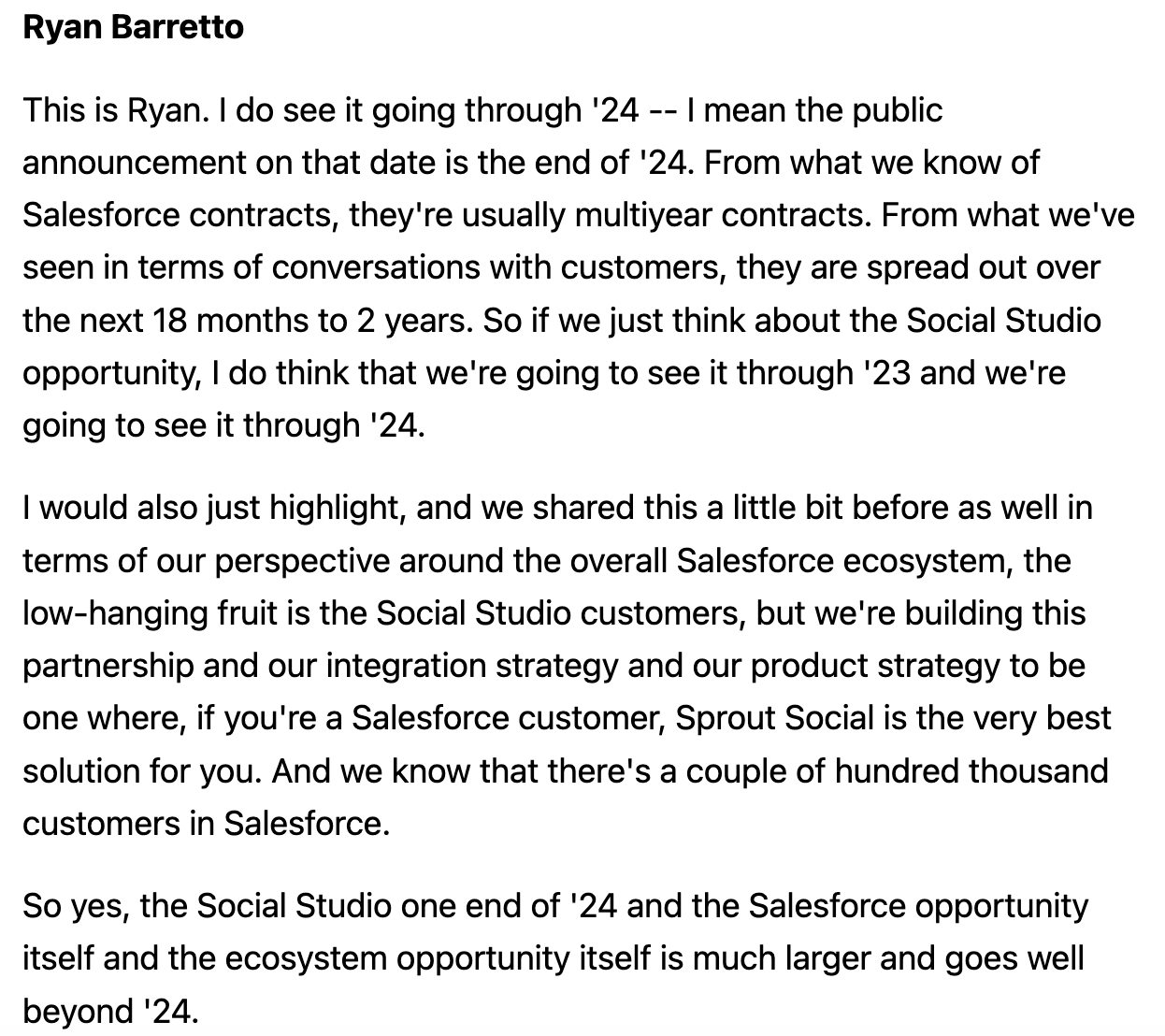

and another reply to a SS question..

I'm gonna be polite about how I characterize these answers. I think my report provided ample evidence with respect to when Fortune 100 SS moved. But just to use some common sense, if SMM was mission critical to an enterprise and SS has not invested in it in YEARS. You are likely the first people to move off of it. He is somehow arguing the biggest will be the last???

As for the Salesforce customers are "typically on multi-year contracts" statement.....

Salesforce is a public company so you don't need to speculate here. As per their disclosures, at least 50% of their subscription rev is on annual duration contracts. (I would also point out that SFDC has some super long-term contracts well over 3 years in their RPO/CRPO mix.) And even if you were not intimately familiar with Social Studio, based on how the product was packaged and priced you would guess that their annual duration mix was higher then the 50-60% total SFDC annual mix.

I would also remind Sprout management that Salesforce stopped renewing multi-year contracts well before the Aug 1, 2022 end of annual renewals. So, if you had a multiyear renewal that landed in early 2022, that became an annual and would be expiring by August 1, 2023. So, just doing some simple math based on SFDC disclosures would have 50-60% gone by probably July 1, 2023 on annual duration mix in line with all SFDC, any multi-years that terminated between Aug 1,2022- Aug 1,2023, and any multi-year who renewed between Jan 1, 2022 and Aug 1, 2022 who could only extend 1 year. So, really they are talking about just new customers who signed with Social Studio on multi-year in 2021 after everyone knew SFDC was not investing in it and had multiple other better alternatives. Thus, their comments are not just misleading, they come off as totally uniformed SaaS executives.

I also really liked this question out of the MS Analayst...

Elizabeth Porter

Got it. And then just as a follow-up, I recognize it's early to be thinking about 2024. But can you shed some incremental light on the drivers that you expect to provide that durable growth against potentially a harder comp just as pricing changes in Social Studio benefited 2023 growth. I know you highlighted some factors like a bigger TAM. But just how quickly can those play out as it relates to 2024 growth? And what are some more specific drivers of your confidence?

Joe Del Preto

Yes. This is Joe, Elizabeth. Happy to answer that. I think what gives us the confidence here is really what we've kind of been talking about is our move up into the mid-market enterprise and the investments we're making. If you think about it, we've just started making those investments over the last like 12 months or so, and it's probably the area where we're hiring and focusing the most.

If you look at, for example, the 50% increase in net new ARR from enterprise, if you look at the fact that our new ACVs across the organization doubled on a year-over basis, we just feel like the deals we're getting into now are much larger, and we believe we're just scratching the surface of that part of our business and those investments.

And so as we get into the back half of this year and we get into 2024 and then we also think about, for example, some of the investments we're making on the R&D side and the momentum we have in customer care and social listening and some of the other things that we've talked about, we just feel like the growth that we're seeing in the most healthy part of our customers, and then we also look at the NDR that were driving the expansion of those customer base, I think all of those give us a lot of confidence going into 2024.

Basically, a non answer from mgmt, which is better then reiterating 30% growth for 2024 and 2025 again. But as you can see they essentially tripled down on SS to hit their 2023 guide, but don't seem to have given any thought to how that would fall apart into 2024 linearity wise and comp stack wise.

They also had some mind boggling comments on RFP's as well as just basically inaccurate comments on what is real-time going on in the competitive landscape.

Anyway, they pretty much tripled down on SS being their whole story for 2023 and really leaned into this we are intentionally shedding SMB's in favor of super valuable enterprises narrative while at the same time reporting their worst $50k+ adds in 3 years. No need to try and rationalize any of this because none of it really makes any sense and is just optic stuff like the 25bps raise to pretty much buy time. Obviously that's not going to work. I also think to the extent you believe they believe what they are saying and its not just them managing the growth cliff impact to the street; the whole business is in serious jeopardy from here as the competitive dynamics have notably ramped since Sprout essentially started running their business for SS low hanging fruit and to try and support a bubble share price.

I now have 1000% confidence this stock is going to see $15-$25 this year.