Razor's Edge: In Defense of Mclovin.....Again...

Applovin really is popular in the activist short community huh?

They are now the undeniable title holder with respect to activist short reports with basically 4 in span of five weeks as well as Lauren's extensive work on the name.

Now, I have a ton of respect for several of the folks involved with the Mclovin short work and I know some of them well. I also know some of the folks defending Mclovin very well. So, this thing is already great market content for me to comment on.

And then you have my own 2c on Mclovin which has been long biased fundamentally, but also with two notable trade short bets on it in the recent chaos. That kicks it up another notch.

Then you have my thoughts on "Edge" investing and the fact that I'm presently short digital ad biz in doximity with a main thesis driver of relative valuation versus peers like App, Reddit, Meta, Zeta.

So, has MW brought anything new to the table?

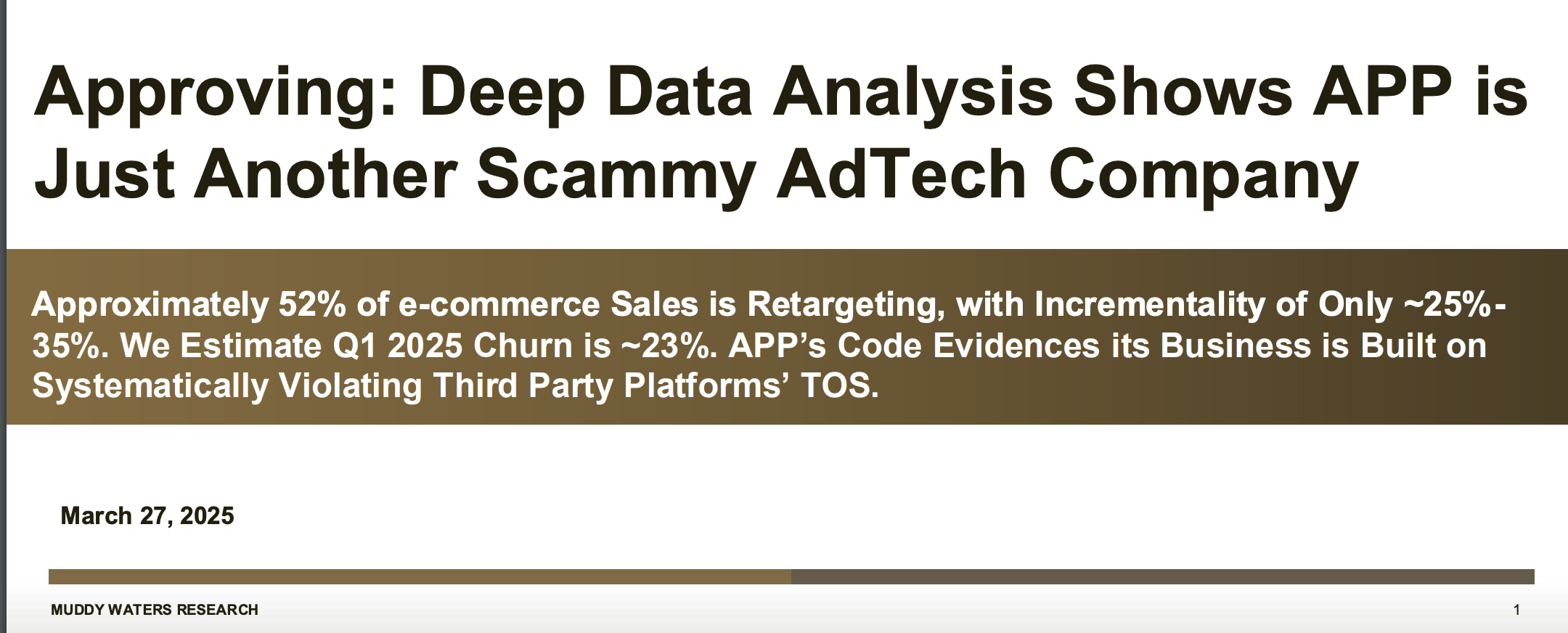

This is the headline...

And they just dive in from there as if the entire business up until the ecom pilots started wasn't the mobile gaming UA biz. Basically, forget about the mobile gaming UA biz which generates 90%+ of the ebitda today, and let's just discuss why ecom ads is doomed.

That's fine as ecom is kind of a big deal going fwd to what the stock is worth, but their conclusion as far as financial context is to take their ecom analysis and compare Applovin to Cheetah Mobile and Zynga w/o ever talking mobile gaming UA.

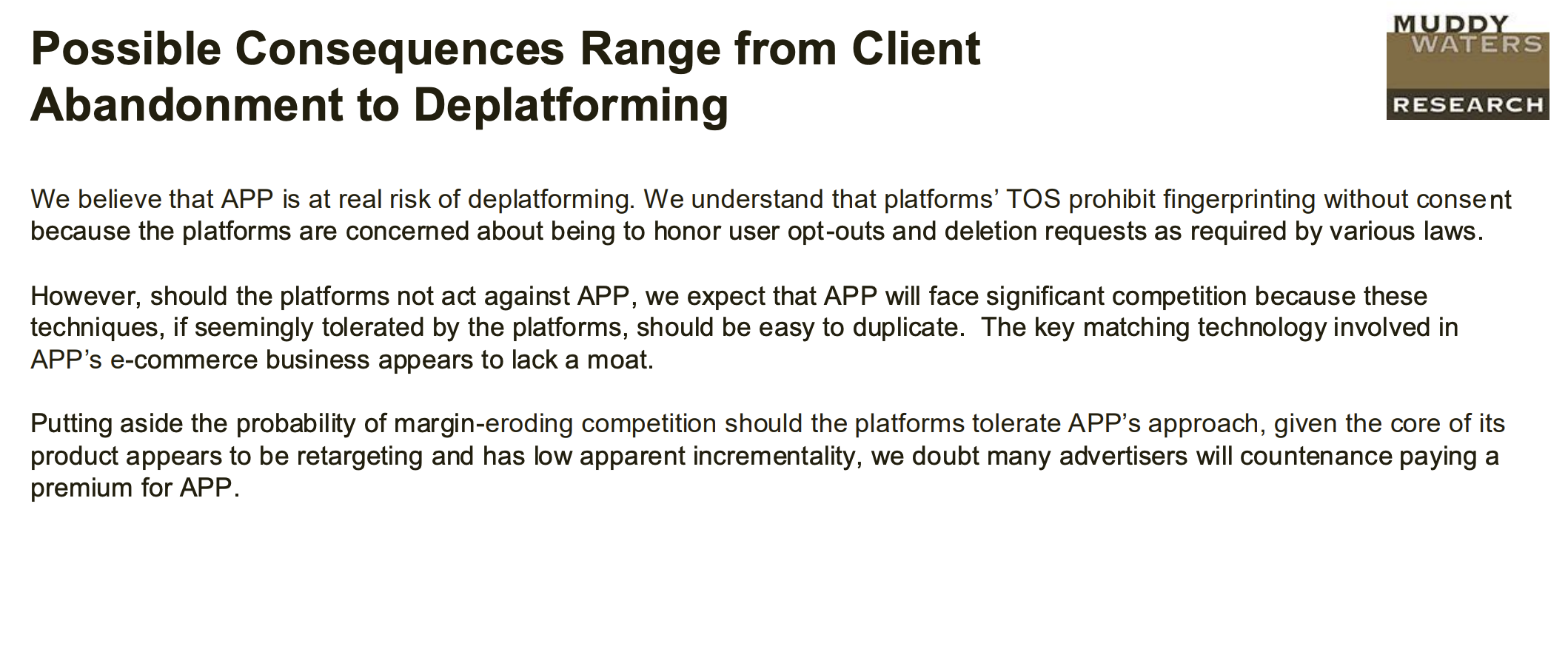

Here is the investment conclusion slide:

So, basically 3 things...

1) Deplatformed and essentially implying but not stating biz is then worthless

2) Not deplatformed and copied which means not worth a premium

3) Even if u can compete it doesn't work well so advertisers won't pay much for it

Anyway, anyone who has read my past takes on this drama knows that the core biz is simply ROI driven with no loyalty. Applovin has basically demonstrated they are very good here to the point of essentially OWNING THE MARKET.

And on point three, Applovin has started out with some of the most sophisticated advertisers on earth as pilot customers. So, I don't really know how that is a point, beyond saying we shall see what they think about this as time passes. Again the question with App is can they replicate their success in mobile gaming in ecom/ctv. So, why not ask the ad spending giants what they think....

This guy has done good work on this topic...

So, far the big spenders seem happy with the perf and are upping spend. Shein/Temu are not stupid when it comes to ad spend.

So, you basically are back to this kind of high level take that Mclovin is gonna get deplatformed by Meta/Google/Apple? before their ecom biz gets going w/o any sort of analysis on why this has NOT HAPPENED IN MOBILE GAMING UA.

Again you basically have skipped over the core and just kind of moved to ecom deplatform=cheetah mobile. You can call that what you want.

So, what about the ecom issues and the data analysis....

I read the report twice and I instantly was surprised by the ATT VS Web Browser tracking issues underpinning their core critical terms of service violations argument. Again this report pretends mobile gaming UA isn't the whole biz so not a shocker they would screenshot web browser tracking and argue Mclovin is violating ATT. This is like 101 level stuff and if this wasn't a firm whose track record warrants immense respect, I would basically say you should just ignore the rest of it.

Now when you talking ecom ads mobile apps and browsers is pretty much the story and for the browsers that is ITP on IOS and NOT ATT.

So, we have clear TOS and data showed mismatch. Also, pretty much everyone with deep knowledge in mobile gaming UA is aware that Mclovin got a fingerprinting leg up pre 2023 changes by Apple and that this is now part of Axon's moat.

As for Meta, the main argument against the ecom ad platform is that its basically over inflating perf attrib and their is TOS violation on MetaAudienceNetwork cause they are collecting the random token identifiers to create a persistent identity graph.

I can say at the surface level the latter claim is not one I can speak to in detail, but as these tokens randomly generated and expire daily on IOS; I kind of don't get the TOS argument. As for the attribution part, which is more important, you basically need to be a MEGA META SPENDER to get into the pilot. So, why would Applovin create that requirement to then deceive the worlds most sophisticated digital advertisers?

And then we go from this to Cheetah which was legit doing click commissions/ingestion and essentially was transparent spyware?

That's a not great bob look.

So, that's my 2c on all that, and now onto the interesting stuff.

I purchased 6 figures worth of App weekly puts when the stock printed 350 on tuesday with a thinking the name will continue to have a valuation ceiling commiserate with more long-term takes on adtech domination for a platform with no community of users essentially. These would have hit a nice 7 figure number near the close yesterday but I had sold them on wednesday after a few percent drop.

But the why on App puts wise there for someone whose been a fan of mgmt and execution I think says more about why the short has been so popular for activists. It's a big liquid name which near 80% ebitda margins that has been hypergrowing and now chasing even larger potential markets.

I think there is a sensible view that at over $50bl an adtech arb platform is going to have a hard time trading at over 20x fwd FCF w/o clear ways to assess the TAM/GDP of the ecosystem. Also, when competition has failed so miserably, the view becomes that maybe one day they figure shit out. So, presently App is high teens fwd 12month ebitda with ebitda essentially expected to grow 60% more. Seeing as you near 80% ebitda margins that basically means you underwriting 60%+ topline growth here. So, yeah picking on this 500 was great. and again at $350 till there is cemented evidence on the type of trajectory you going to get out of ecom.

Now imagine trying to risk manage 5 short reports with that thesis?

Or being like well 45x ebitda is still risky even if 2025 goes to plan because by summer you are asking about 2026 and effectively having the same convo over and over till a step function change is clear in ecom or its lack there of is cemented.

This is the type of shit the actual thematic bulls worry about and the very questions many were asking when the stock was at $70 and a single digit ebitda multiple. So, you don't need much to remind them this rental at this level could reset notably downward.

And this is kind of part of the issue/challenge with activist shorting these days.

A report on what the business is worth without drama is not going to move the stock in a window where you confidently eliminate market risk (even that might be an illusion). Also, everyone has A.D.D these days so you need to work to get attention to substance. That's fine. But i think the cost of that is people totally disregarding fundamental shorts, and I think I have proven that consistently over the past 10 years. You can short good and even great businesses and win if you get deep enough into the biz and space and still recognize that you have plausible uncertainty. The shitco shorts w/o doubt on the future actually turn out to be way harder to risk manage.

I have shorted Doximity largely knowing they have done well execution wise and benefit from digital tailwinds, but talking to a very large sample of their largest customers has given me confidence the biz is relatively mispriced. And yes there is data about doctors long shifting to sermo and linkedin being aggressive and AI really being a concern going fwd etc, but the starting point is I think the stock can fall 40% w/o any of that mattering and pointing to tons of names that back that thinking up relatively.

This same thinking has spurred two App short counter long trades and I personally have vetted so many takes industry wide on just how amazing these guys are execution wise. So, things can be right for the wrong reasons, and that's what makes the market great.

p.s. -didn't have time proof this much so factor that into ur reading....